As we usher in the new year, global financial markets have no shortage of geopolitical issues to contend with in 2026. Before we look ahead, let’s look back at 2025. The geopolitical laundry list of significant events in 2025 included the Russia–Ukraine conflict in its fourth year and Donald Trump returning to the presidency, signing 225 executive orders in his first year and imposing sweeping tariffs on US trading partners. Syria’s Bashar al-Assad’s regime fell, a ceasefire ended roughly two years of fighting in the Israel–Hamas conflict, one of the worst humanitarian crises in history raged on in Sudan, and a border conflict erupted between Cambodia and Thailand. As we speak, former Venezuelan President Nicolas Maduro sits in a New York City jail cell after being arrested early Saturday (January 3, 2026) by US forces.

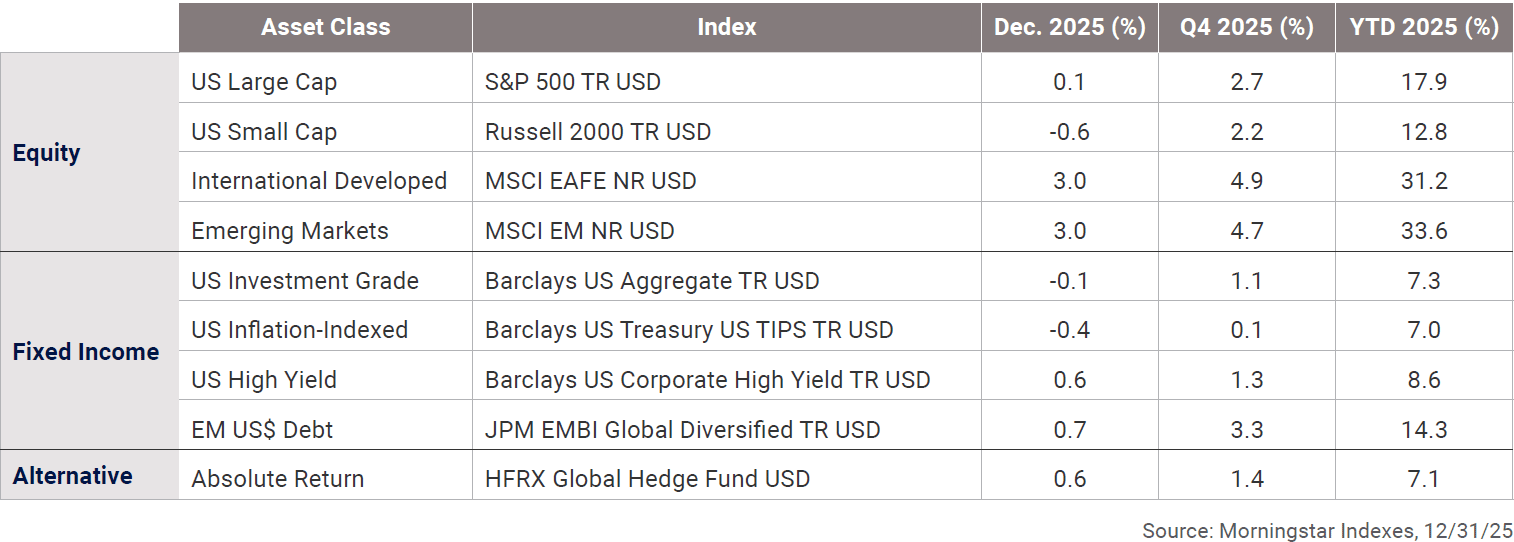

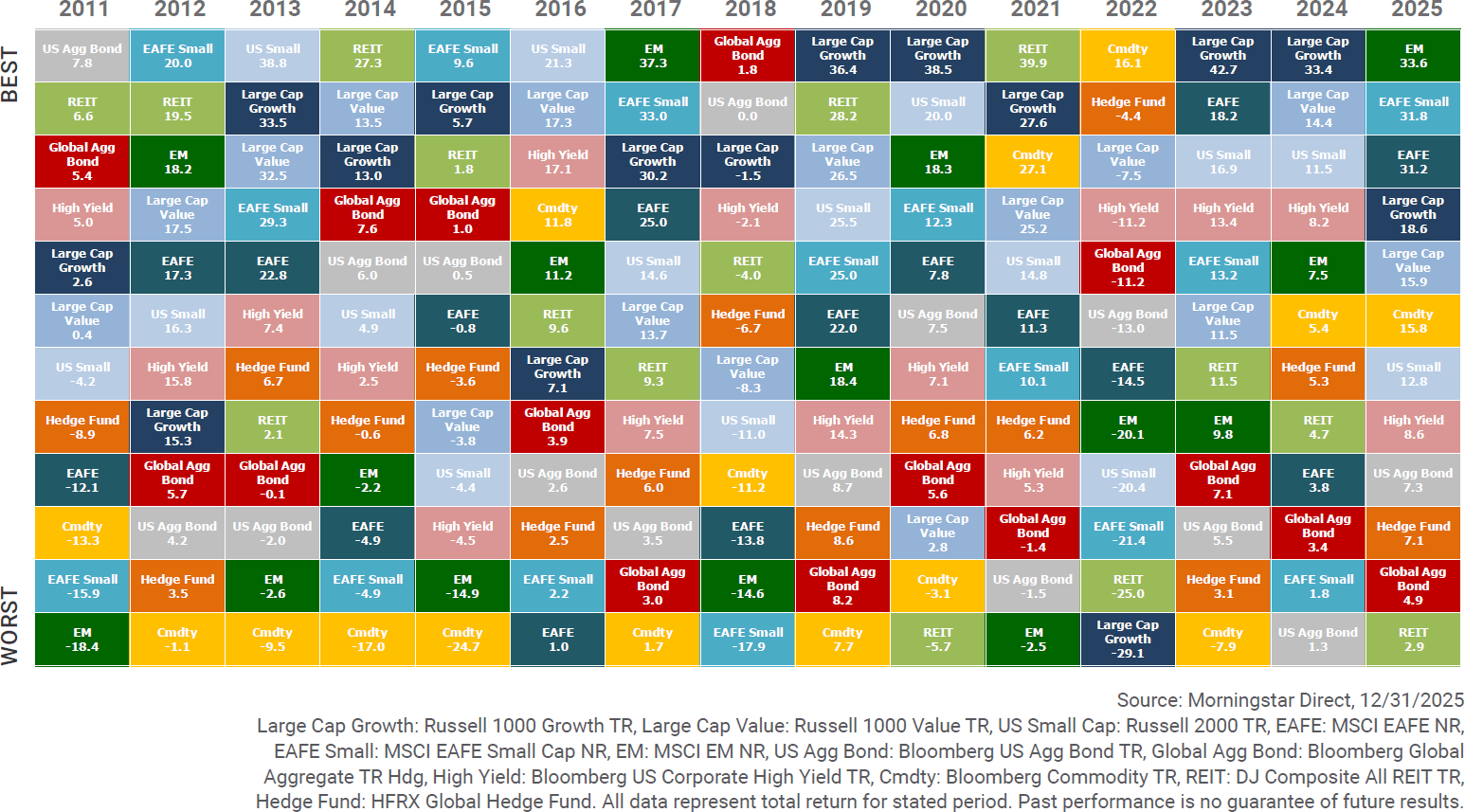

Despite a -17.5% decline from February 19 to April, 2025, the S&P 500 returned 17.9% for the calendar year 2025. International equities, both developed and emerging markets, surged 31.2% and 33.6%, respectively, leading all equity categories for just the second time in the last 15 years.

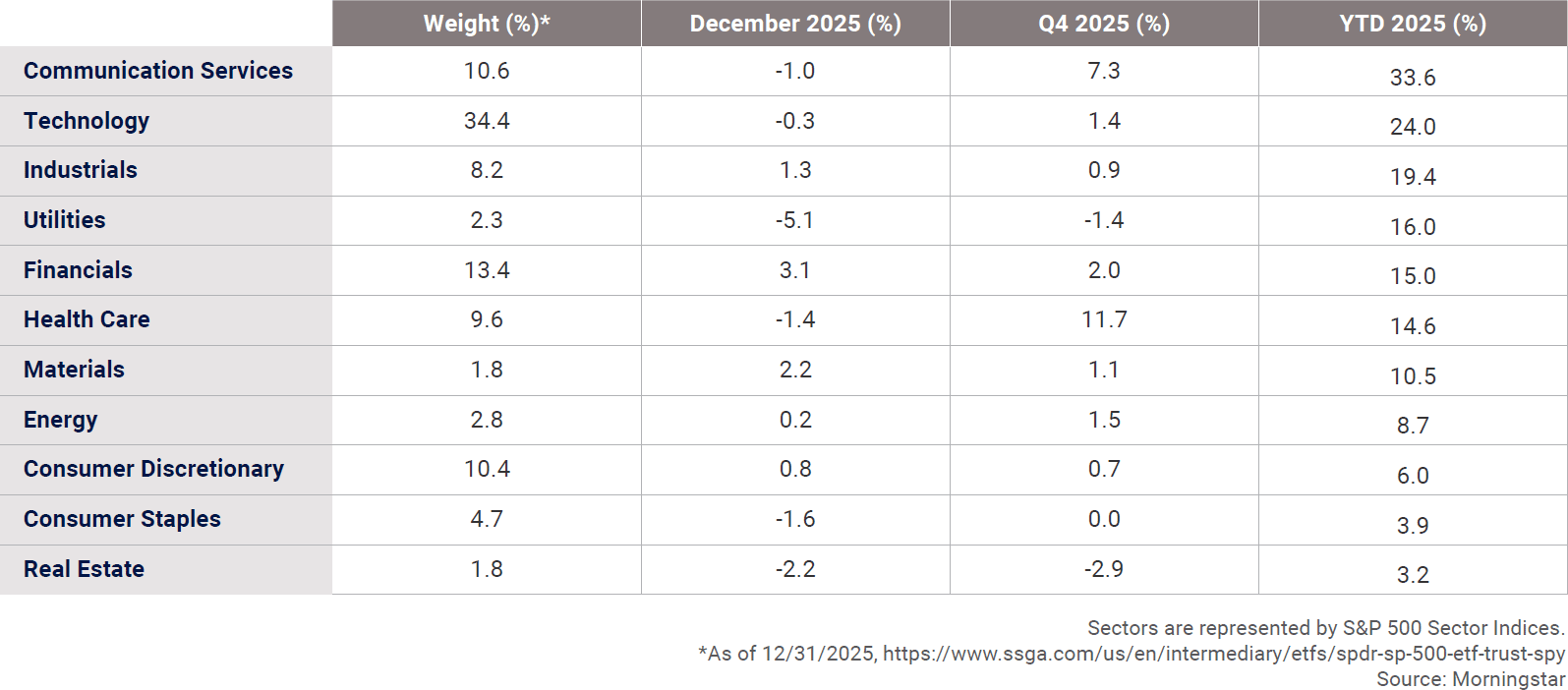

As illustrated in the chart below, Communication Services and Technology led the way in 2025 just as they had in the previous year. However, it is notable that every sector finished 2025 with a positive return—ranging from 33.6% for Communication Services to 3.2% for Real Estate.

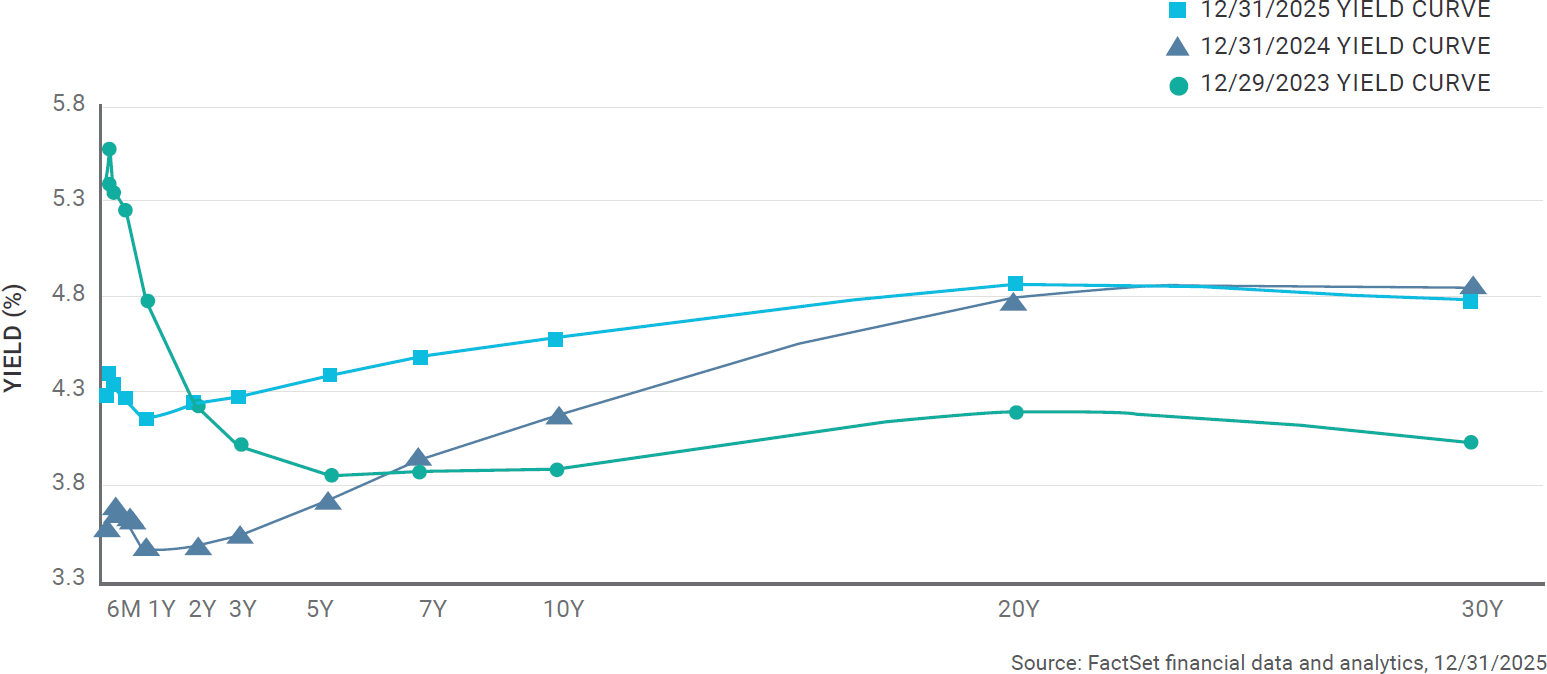

The remnants of the Covid-induced yield curve inversion unwound over the course of 2025. With the 10-year Treasury bond yield currently at 4.29% as of 1/20/2026, the likely path for longer-term interest rates is higher. We continue to focus on bonds with short maturities, keeping portfolio duration shorter with more emphasis on credit to drive returns.

In addition to our conservative bond positioning, we continue to believe strongly in the value of diversification provided by liquid alternative strategies, where we work with managers who provide uncorrelated sources of return and greater stability during market volatility.

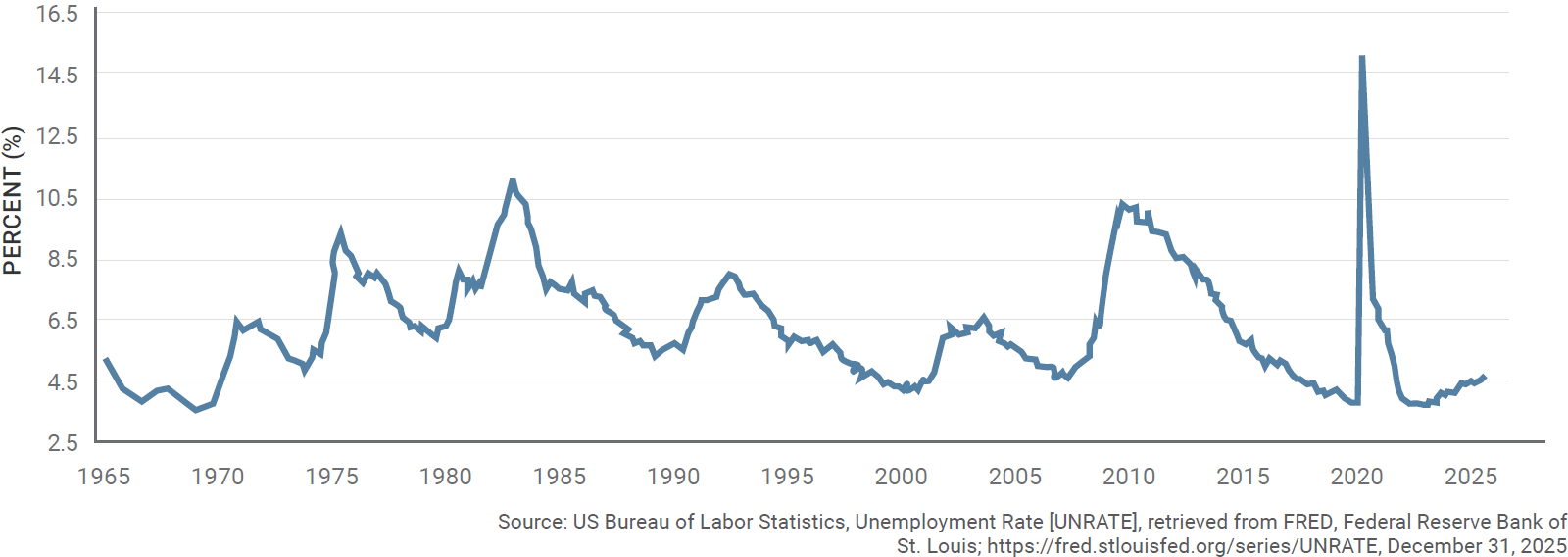

The employment picture for 2026 has been clouded somewhat by immigration reform. The flow of migration over our open borders has slowed significantly, but it hasn’t put the brakes on growth in the US labor force. As foreign-born workers exit the US labor force, native-born Americans are filling the void, which should keep the unemployment rate in the 4.4% to 4.7% range this year. Meanwhile, the participation rate of prime-age workers (those 25 to 54 years of age) sits above pre-pandemic levels. With prime-age workers near full employment, demographics (baby boomers retiring, etc.) will keep the overall participation rate (currently 62.5%) below its pre-pandemic (63.3%) level. Despite tepid job gains of late, companies are holding on to existing workers and layoffs remain low. The most recent weekly Labor Department report showed that new claims for unemployment benefits fell 16,000 to 199,000. This was the third consecutive weekly decline, and claims sit among the lowest levels over the past 12 months. In addition, continuing claims for those receiving ongoing unemployment benefits fell 47,000 to 1.87 million. (Source: FactSet 12/31/2025)

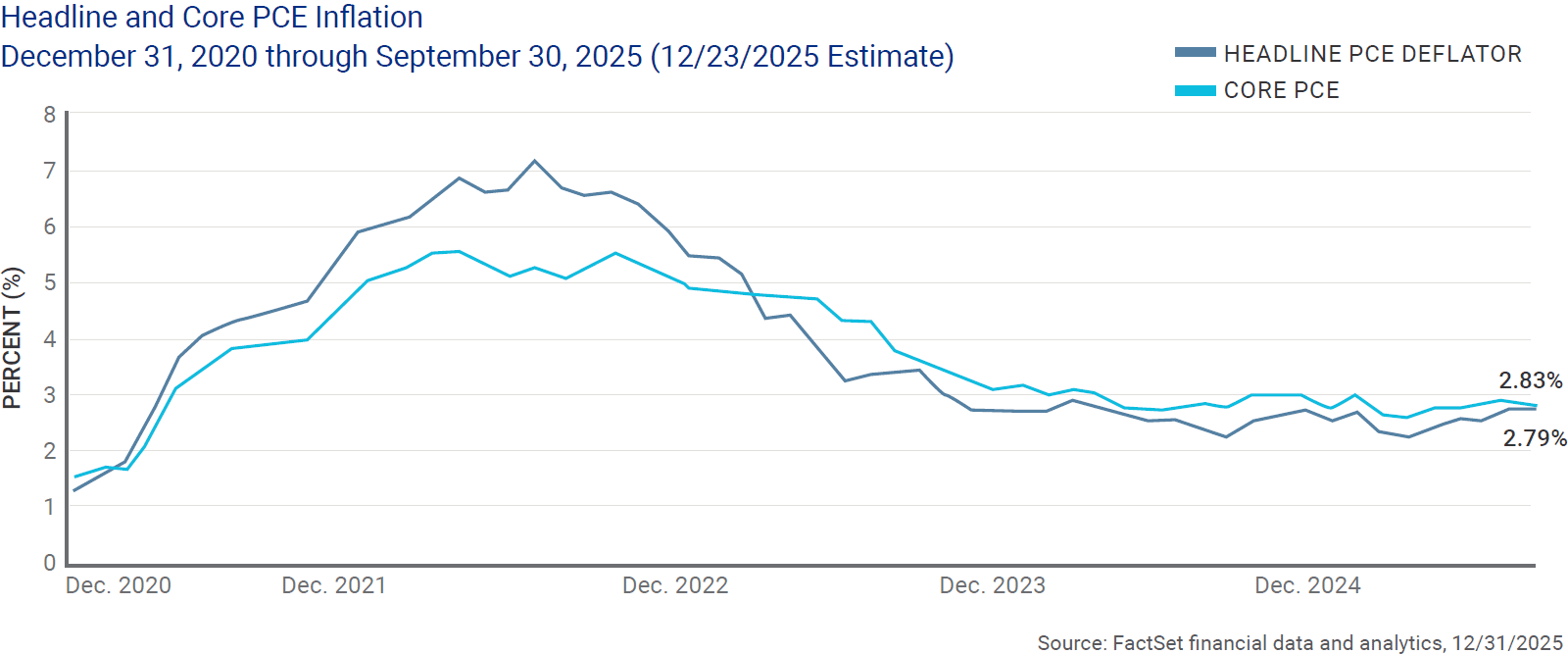

Inflation, and The Federal Reserve’s preferred inflation metric (the PCE index), remains stickier than we anticipated. Core and Headline PCE both currently sit at 2.8%—still a fair bit above the Fed’s 2.0% target. With costs moderating each month for shelter (housing, rents) and energy, along with sluggish growth in the US money supply (M2), we anticipate continued improvement in the PCE index as the year progresses, but it will probably remain slightly above the Fed’s target for most of the year, arguing against multiple rate cuts.

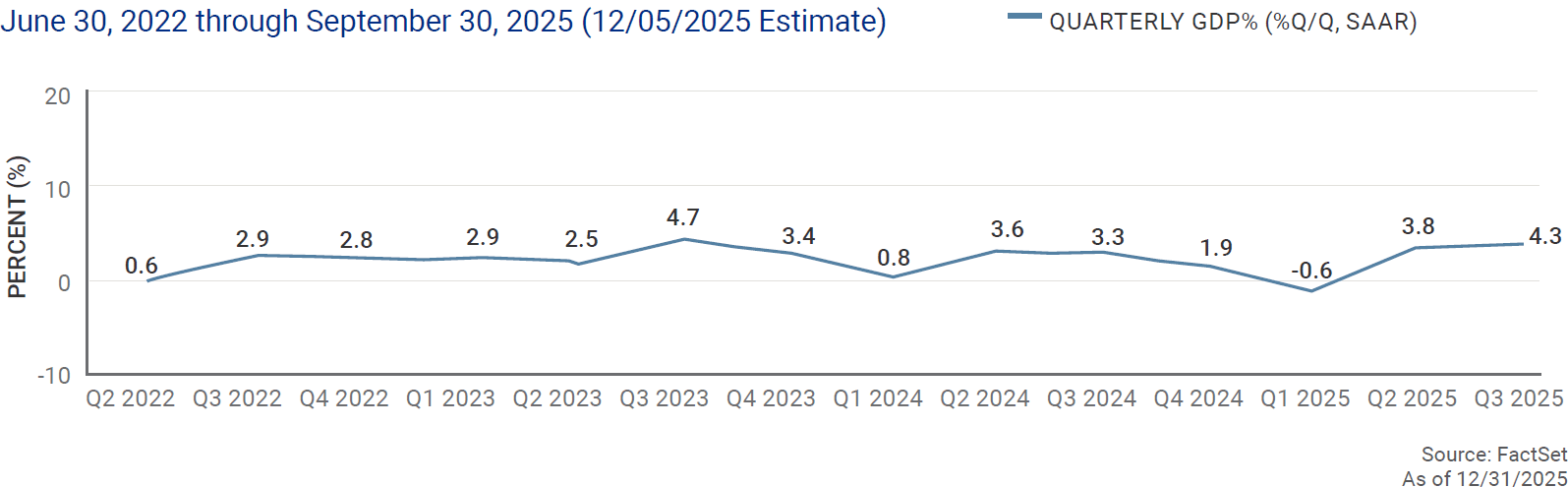

Real (inflation-adjusted) GDP followed up Q2’s 3.8% increase by rising 4.3% (annualized) in Q3—the fastest pace in two years—led by a 3.0% increase in consumer spending combined with private fixed investment. The tariff-induced slump in Q1 coupled with the federal shutdown in Q4 likely slowed annual GDP growth in 2025 from 2.8% in 2024 (we will get a first look at Q4 GDP in early February), but 2026 should see a bounce back in growth, led by continued consumer spending and technology-led productivity gains, which could pull GDP growth back above 3.0%, since both fiscal and monetary policy in the US should prove stimulative for growth in 2026. (Source: FactSet financial data and analytics, 12/31/2025)

No single theme has dominated the investment conversation (or proportion of investor returns) the last two and a half years like artificial intelligence. Companies large and small are investing significant amounts of money into AI, and market participants are trying not to miss out. Like most, we agree the opportunity set is massive. AI has the potential to dramatically alter how firms in every sector do business and interact with their customers. We are already seeing that its impact will go well beyond technology firms.

Estimates as to the scale of AI’s overall economic impact vary, but most are staggering. For example, a PWC study places the financial impact at a total of $15.7 trillion to the global economy by 2030 (Source: PWC 2026 AI Business Predictions. https://www.pwc.com/us/en/tech-effect/ai-analytics/ai-predictions.html). The impact is also already being felt—AI investments contributed roughly two-thirds of GDP growth in 2025 (Source: Lazard Global Outlook 2026. https://www.lazardassetmanagement.com/us/en_us/research-insights/investment-insights/investment-research/global-outlook-2026).

While our clients have been rewarded handsomely the last few years as a result of AI-related investments, it is only natural to start wondering if the dreaded “B word” (bubble) will present itself in 2026. We believe it is crucial to stay invested in AI-themed investments across multiple sectors. We are both sticking with those that have previously worked and actively looking for new opportunities. However, it is also true that nearly every transformative technological change in history—from railroads to radio to the internet—has also come with a period of digestion and consolidation (call it a “bubble” if you must). There will be inevitable growing pains as we move from the initial “unlimited optimism” phase to more questions about how and when actual profit will come. What we may see as early as 2026 is some differentiation between “AI winners” and “AI losers” as the theme continues to mature and evolve over time. For example: will the winners today be the ultimate winners when it’s all said and done, or will some fall by the wayside and new entrants take their place? Remember that some of the early winners in transformative technologies like internet adoption (e.g., Prodigy, MySpace) as well as automobiles (e.g., Packard) did not survive the test of time. It would be logical to expect the same here.

So, while we want (and need) to stay invested in the AI theme, we also need to manage it actively for our clients as we move into 2026.

The initial market reaction to the Maduro arrest appears to represent the optimistic scenario where US intervention results in successful regime change, substantial political and economic reconstruction proceeds smoothly, and oil production eventually recovers. Chevron and Exxon Mobil have surged in the early days following the arrest. However, significant downside risks remain around political instability, legal challenges to the operation, implementation details, and whether Venezuela can avoid another cycle of hyperinflation and economic distress. The repercussions may be felt far and wide: Will this action embolden China to take more aggressive actions in Taiwan? Will Putin seek control in the Baltic states?

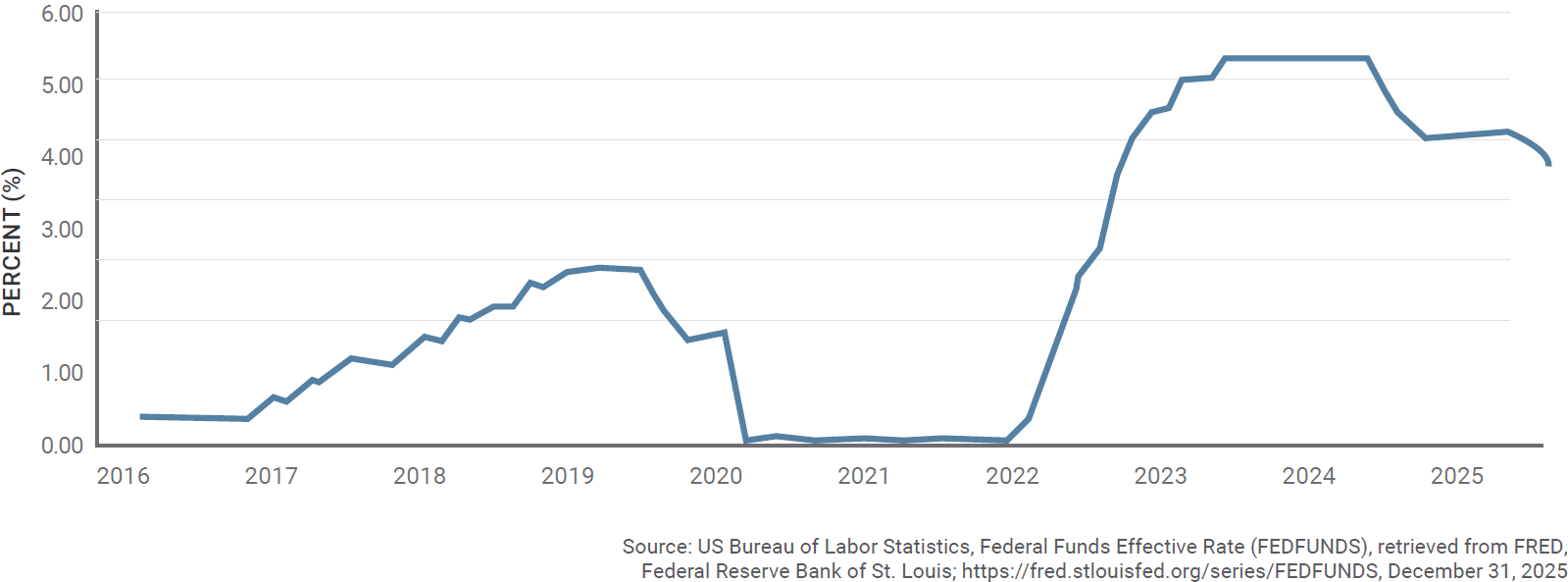

At midyear 2025, we wrote about the expectation for three rate cuts in the second half of 2025, and that did in fact come to pass. The Fed lowered the Fed Funds rate by 25bps in September, October, and December, bringing the Fed Funds rate down from 4.5% at the beginning of 2025 to 3.75% on 12/31/2025. As of year-end, the market is pricing in two additional cuts for 2026 (one midyear and one in the back half of the year). These additional cuts would certainly be welcomed by the market, but there are risks to this outlook. For starters, Fed Chair Jerome Powell’s term ends in 2026 and President Trump will get to appoint a new chair. This isn’t necessarily a problem, but it is abundantly clear that President Trump is trying to influence Fed decisions more than any president in recent history. Political preferences aside, a less independent Fed would not be a good thing for markets. Former Fed Chair William McChesney Martin is credited with the famous comment about the Fed “taking away the punch bowl when the party was really warming up.” Continued rate cuts in the face of accelerating GDP growth might make a politician look good in the near term, but the ramifications on overheating inflation can’t be ignored. The perception of a “biased” Fed would also lead to less credibility for the US dollar, monetary policy, and interest rate regime. With the Fed Funds rate currently at a range of 3.50–3.75%, the Fed still has plenty of ammunition for additional cuts should growth falter and/or the labor market deteriorates further.

There was a “perfect storm” of dynamics that resulted in 2025 being only the second time in the last 15 years the Developing International and Emerging Markets were the best-performing asset classes for the year.

Those dynamics included a weaker US dollar, the AI boom, NATO policy changes, a stable European banking system, and relative valuations.

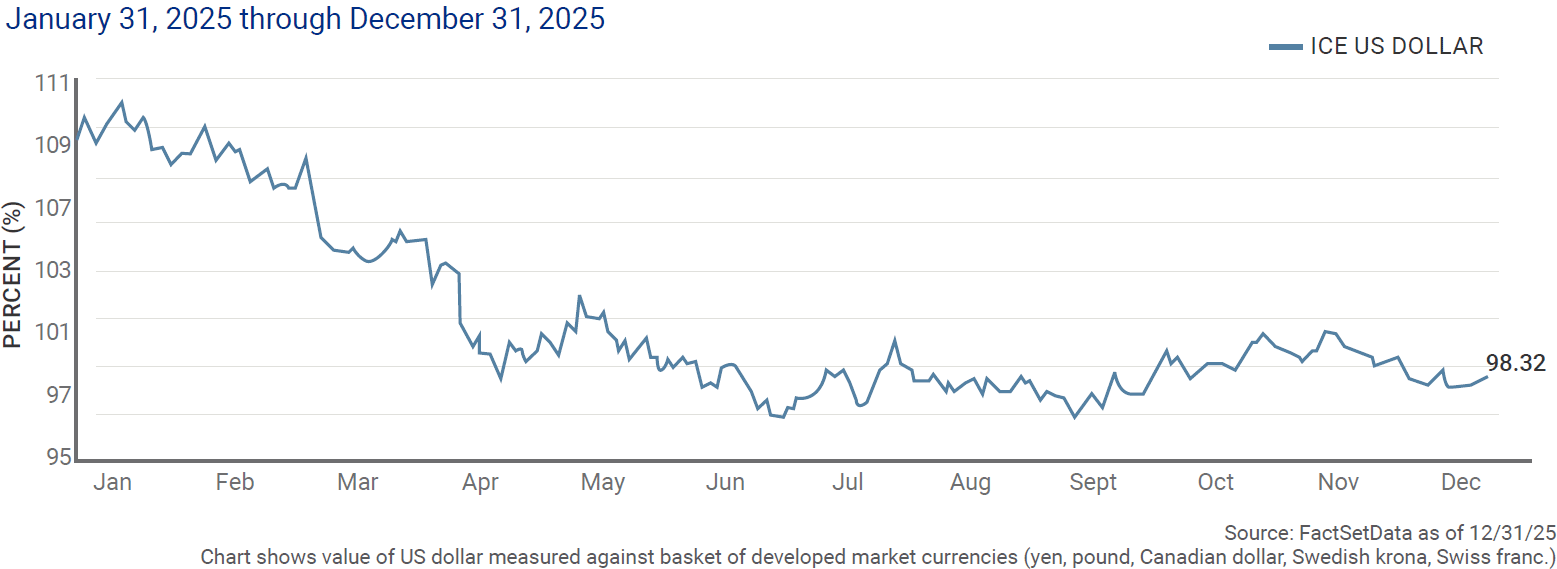

The ability for investors to confidently navigate the investing backdrop dramatically altered due to the way the tariff policy was rolled out. What started as a broad-based, uniform tariff strategy quickly evolved into a “case-by-case” or “countryby-country” negotiation, creating uncertainty around imports, exports, and inflation. Also, realistic concerns have been developing related to the US budget deficit and potential politicization of the Federal Reserve. Hence, investors have become less confident in our nation’s currency, leading the US dollar down -9.4% in 2025. US dollar weakness resulted in non-US assets becoming relatively more valuable, but it also makes US exports cheaper for foreign buyers.

Similar to the United States, Europe and Asia have plenty of beneficiaries from the AI boom. South Korea’s Kospi Index was up 76% and Japan’s Nikkei 225 was up 26%. Specific stocks with great returns included Kioxi, a Japanese memory chip maker which was up 536%; tech conglomerate Samsung was up 130%; Taiwan Semi which increased 46%; and Alibaba, which launched an AI chatbot, driving its stock higher by 76%.

In June, NATO pledged to ramp up defense spending to 5% of GDP by 2035. This should prove to be a catalyst as there are some large European defense manufacturers that will benefit and there will likely be tangential investment in infrastructure such as rails, roads, and bridges.

The European Central Bank’s decision in mid-2025 to stop reducing rates resulted in stable but elevated rates, a nice environment for banks. That combination as well as cost cuts and better than expected economic growth resulted in very strong performance for European banks. As a result, the Euro Stoxx Bank Index was up over 70% in 2025.

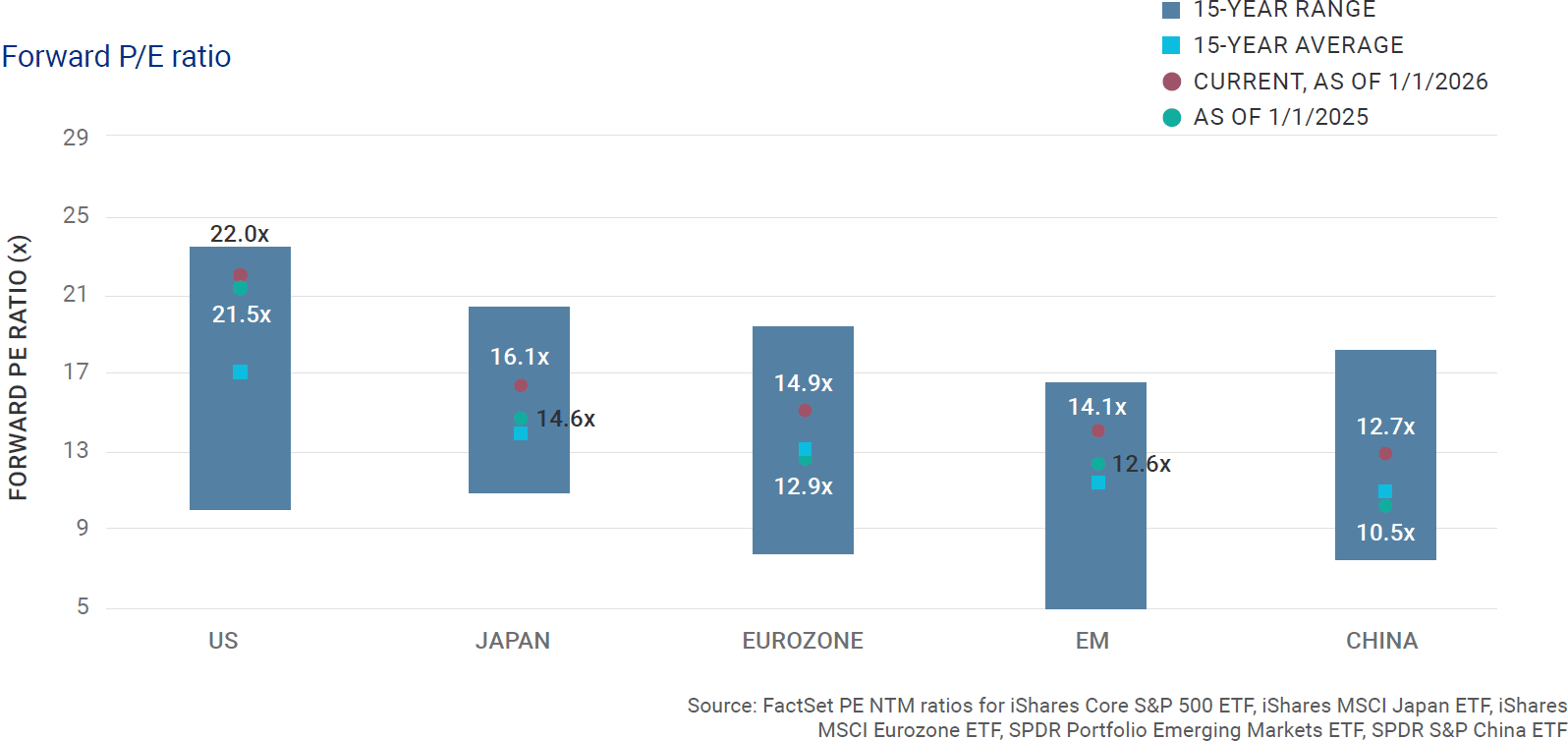

Relative valuation at the start of 2025 heavily favored international markets and continued as we entered 2026. This proved attractive to investors, many of which were heavily underweight for many years as international markets were trading close to the midpoint or much lower of their 15-year forward P/E ratios versus the United States trading at the high end of the range.

We expect the trends highlighted above (policy uncertainty, AI boom, NATO spending, ECB outlook, and relative valuations) to continue into 2026. Hence, we expect international and emerging markets performance to continue to be strong and to maintain our current exposures.

While 2026 is likely to present numerous challenges, we are well-positioned to benefit from positive developments while managing downside risk should things not go according to plan. Remaining disciplined and focused on long-term goals is key to investment success. Market fluctuations are a normal part of the journey, and reacting emotionally to short-term moves often does more harm than good.

This was produced by Webster Bank, National Association (“Webster Bank”). The information is of general market, economic, and political conditions or statistical summaries of financial data and is not an analysis of the price or market for any product or transaction. Under no circumstances should the information be considered trading advice or a recommendation or solicitation to buy or sell any products or services or a commitment to enter into any transaction. You should consult with your own independent advisors before taking any action based on the information.

The information and opinions presented are current only as of the date of writing, without regard to the date on which you may access or read this information. All opinions and estimates are subject to change at any time without notice. This material may not be reproduced or redistributed without Webster Bank’s express written permission.

Investment, trust, credit and banking services are offered by Webster Private Bank, a division of Webster Bank, N.A.

Investment products offered by Webster Private Bank are not FDIC or government insured; are not guaranteed by Webster Bank; may involve investment risks, including loss of principal amount invested; and are not deposits or other obligations of Webster Bank.

Webster Private Bank is not in the business of providing tax or legal advice. Consult with your independent attorney, tax consultant or other professional advisor for final recommendations and before changing or implementing any financial, tax or estate planning advice.

All credit products are subject to the normal credit approval process.